The International Monetary Fund anticipates that the economic fallout from COVID-19 will plunge the world into a recession, the likes of which we have not experienced since the Great Depression. This seems increasingly likely.

Over 30 million Americans have already lost their jobs, and the Federal Reserve estimates that this figure could climb to over 47 million in the coming months. Adding fuel to this fire is the fact that 78 percent of American workers live paycheck to paycheck, and over 30 percent have no savings whatsoever.

There will be lean times ahead. And to whom will Americans turn for guidance? Who will fix the economy? According to the media we should rely on the sage advice of academic economists—“experts.” If they cannot deliver us, no one can.

I hate to break it to academia, but economists are the last people to whom we should be turning for advice about this situation. Why? For starters, their relentless support for economic globalization—for so-called “free” trade—created the international networks which facilitated COVID-19’s rapid spread. More importantly, economists know nothing.

Case-in-point: COVID-19 was the single most important event to impact the global economy since 2008. It has put millions of people out of work. It crashed the stock market. It has fundamentally altered our spending patterns. And yet, a grand total of zero economists—not even one maverick—predicted COVID-19 or anything like it. In fact, it was impossible for economists to predict the pandemic.

This is a big problem for economists—for classical economics generally. If the economy is primarily driven by unpredictable events like COVID-19, which exist beyond the scope of economic models, then what is the point of these economic models? Why should we trust economists wedded to these methods to manage the economy?

Would you trust a blind bus driver? No.

A Picture is Worth a Thousand Words

Economists understand the economy through the application of rules, the interplay of theories, and the manipulation of models.

Knowledge is acquired as follows: economists observe the economy. They notice patterns which they formulate into rules, like the Law of Supply and Demand. Multiple rules are combined into theories, and these theories are then used to generate complicated predictive models. Models which, ideally, tell the economist how the economy ought to—nay, will—work.

Like a child abstracting the shape of a triangle from a mountain, the economist abstracts rules from the marketplace. Of course, the mountain does not really look like the triangle. In fact, no individual mountain ever actually looks like the triangle. The triangle is an abstraction, an idea that does not actually exist. The mountains exist. So too, the economist’s formulated rule does not exist. Only the market exists.

The problem is that economists build their theories from these abstracted rules, and from their theories, models. They then use these models—which at this point have little in common with the actual market—to predict how the real market should behave in the future. This is an exercise in futility. Why?

We cannot predict the particular from the general.

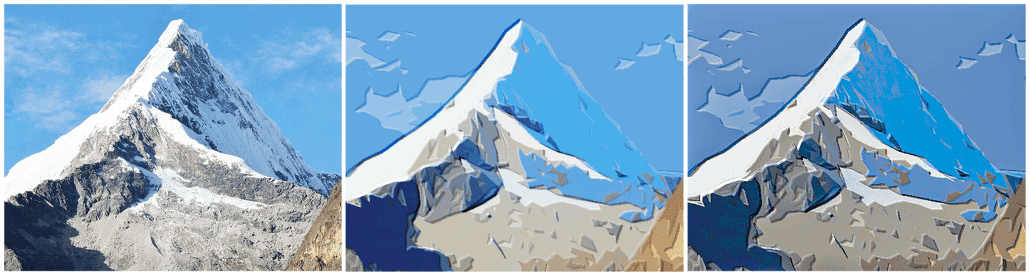

Consider the following visual example.

The left panel depicts a mountain. In the middle panel, the image has been abstracted to show the “rules” governing its composition—its triangular shape. The right panel shows what happens when you try to reconstitute or add additional detail to the abstract image. This is a visual representation of the output of an economic model. It is useless.

Abstraction is a one-way street. One can abstract triangles from mountains, but not mountains from triangles—and this is precisely what economic models attempt to do. They try to predict a specific economic future (mountain) based on general rules (triangles). This is impossible.

If we want to understand what an undiscovered mountain might look like, we should look at previously-discovered mountains, rather than waste our time perusing construction paper triangles with crayon snowcaps.

A Mouth Full of Marshmallows

In 1972 the Stanford psychologist Walter Mischel conducted a ground-breaking experiment. He offered children a choice: one marshmallow now, or two marshmallows in fifteen minutes. The catch? The child had to sit in an otherwise boring room with the marshmallow, mano a mano. Well, mano a marshmallow!

This was a test of will. Could the child delay gratification long enough to reap a bigger reward? Most children failed. They gobbled up their prize with extreme ferocity. But a heroic few strengthened their spirits and resisted temptation. They were rewarded with an ample prize. More marshmallows.

The lesson here is that what may seem like a good trade today—a free marshmallow—may be a bad trade tomorrow. Children understand this problem, they just cannot control their hungry little appetites. Economists, on the other hand, don’t even see the problem.

Economic theories are Platonic constructions. They exist in the abstract realm, independent of physical space, and more importantly, independent of time. As such, they can only purport to tell us what is economically efficient in this rarified setting. This is not helpful because we live in the real world where time horizons matter.

For example, according to the Theory of Comparative Advantage, America ought to buy computers from China because China can manufacture computers cheaper than America can manufacture them. Likewise, America should sell soybeans to China because we can grow soybeans cheaper than the Chinese can grow them. Soybeans for computers is a good deal, according to classical economic theory.

But this is ass-backwards. Soybean farming is a dead-end industry. Meanwhile, manufacturing—and directly tied into this, designing—computers is a growing industry which is more likely to benefit from technological advancement. This is why investment is flowing into technology, rather than into farming.

Summing up: what looks like a good deal today may be a bad deal tomorrow, and vice versa. Businessmen and investors implicitly understand this, and this explains why they are willing to lose money in the short term by starting a business or buying a battered stock—a categorically “inefficient” trade—so that they can make money in the years to come.

If economists were worth their weight in gold, then they would already be worth their weight in gold. They’re not. Investors and businessmen—like Warren Buffet or Donald Trump—are. Time horizons matter.

Butterfly-Kisses or Tornados?

Economists will not—cannot—deliver us from COVID-19’s economic fallout because they don’t even know what the economy is.

Economic models are based on the idea that the economy is like a giant billiards table: the cue ball (supply) interacts with the eight ball (demand) in a predictable way. This allows economists to know how the economy will respond to their simulations. This is false.

The economy is a complex system. In other words, the relationship between cause and effect is not always obvious—X may cause Y sometimes, but not other times. In fact, X may cause Y and Z, or cause an entirely novel effect. Because of this, economists cannot predict with any certainty how a complex system will behave, they can only forecast likely outcomes based on prior empirical observations.

The classic example of a complex system’s unpredictability is the butterfly effect. Imagine a butterfly. It flaps around your garden, subtly disturbing the air. Although initially imperceptible, these small atmospheric changes may give a breeze just enough impetus to blow. This breeze may feed into another, and another—a gust of wind, a gale, a storm. Eventually, a tornado is born of the butterfly’s wings.

The economist would have us believe that he is a new Isaac Newton, who can rearrange the economy as if he were repositioning balls on a billiards table. In reality, he is a poor man’s Al Roker—but not nearly as self-aware.

Not only did economists fail to predict COVID-19—thereby proving that they are blind to the driving forces that shape the economy—but they supported the economic globalization that brought the infection to our shores. And now they expect us to believe that they can “fix” the economy?

We would be fools to trust them.